UAE eInvoicing is now law — everything your business needs to know (and do)

The UAE has made structured eInvoicing mandatory under PINT-AE. Here's the law, the current 3-tier timeline, the integration work, and what your business should do this week.

Contents15 sections · 15 min

- 01What eInvoicing is — and what it isn’t

- 02The UAE’s specific model: DCTCE / 5-corner Peppol

- 03The legal framework

- 04Scope: who is in, who is out

- 05The current timeline

- 06What your invoices must contain

- 07Who does what

- 08The ERP integration work, in eight steps

- 09Where Codelexy fits

- 10The benefits beyond compliance

- 11How to choose an ASP

- 12On penalties

- 13Your next steps — a practical checklist

- 14Frequently asked questions

- 15Closing thought

If you run a business in the UAE and you issue invoices, this regulation affects you directly. The mandate covers every B2B, B2G, G2B and G2G transaction, regardless of whether you are VAT-registered. Missing the deadline carries financial penalties and risks invalidating your invoices.

The UAE has made electronic invoicing mandatory. From 1 January 2027 for large companies, 1 July 2027 for SMEs and 1 October 2027 for government entities, every B2B, B2G, G2B and G2G invoice in the UAE must be issued, exchanged and reported digitally through a government-approved network — in a structured format called PINT-AE.

PDFs are no longer enough. Emailed invoices are no longer enough. Word documents, scans and printable HTML are no longer enough. The mandate is structural — a real, machine-readable format moving over the Peppol network, with tax data reported to the Federal Tax Authority (FTA) in near real time.

This piece covers what eInvoicing actually is, the UAE’s specific model, the current timeline (including the extension introduced by Ministerial Resolution 66 of 2026), the integration work, and how Codelexy helps clients ship the connector that sits between their ERP and the network.

What eInvoicing is — and what it isn’t

| eInvoicing is not | eInvoicing is |

|---|---|

| A PDF emailed to a customer | A structured digital document |

| A scanned paper invoice | In XML, per the PINT-AE specification |

| A JPG / PNG of an invoice | Exchanged via the Peppol network |

| A web-portal upload | Auto-validated at every hop |

| Any printable invoice | Reported to the FTA in real time |

A PDF is a handwritten letter — a human can read it, a computer has to guess. A PINT-AE eInvoice is a database record: structured, verifiable, processable in milliseconds. Per the MoF, the Electronic Invoice will not feature a QR code or barcode — it is XML, full stop.

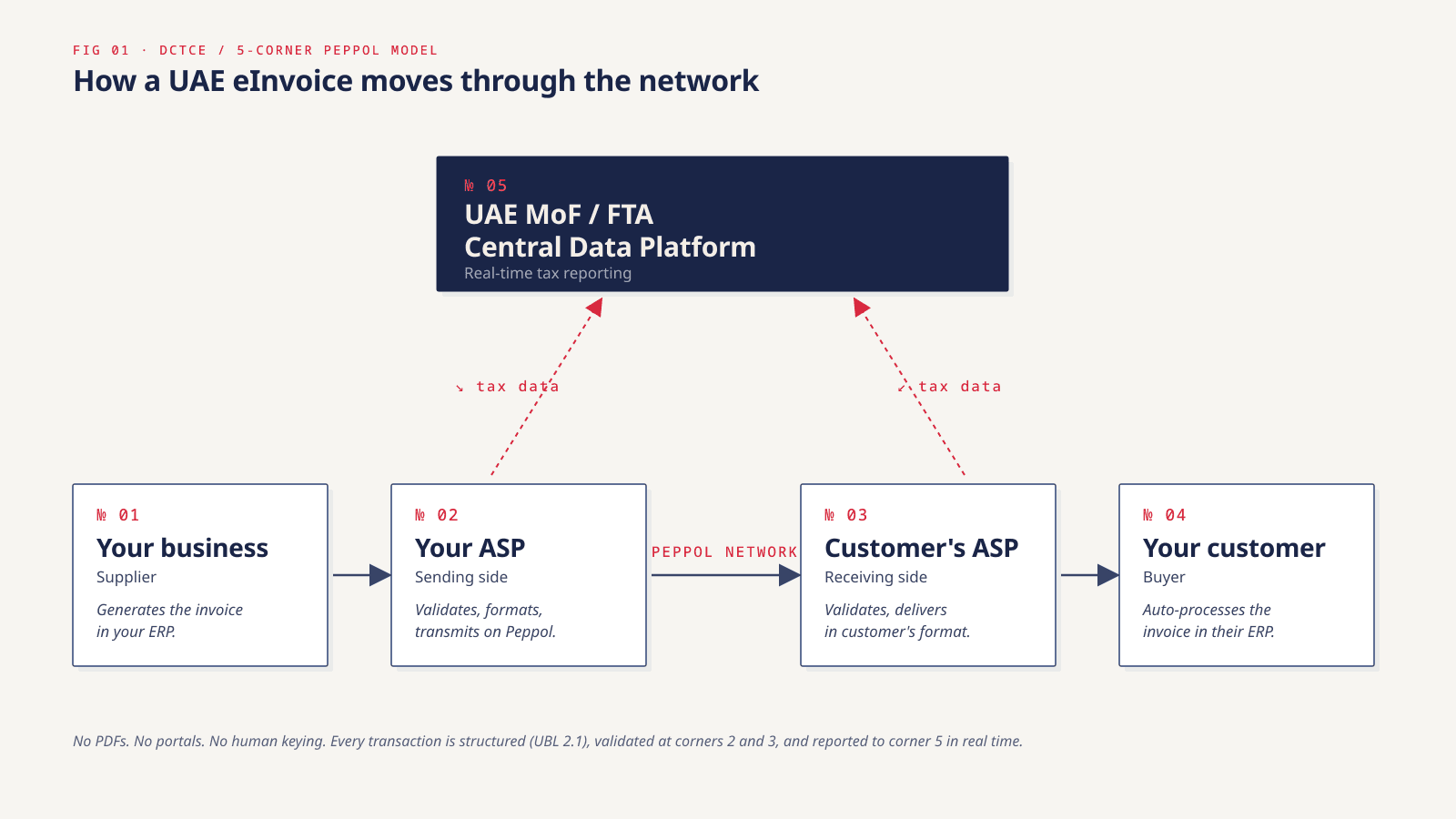

The UAE’s specific model: DCTCE / 5-corner Peppol

The UAE has adopted the Decentralized Continuous Transaction Control and Exchange model (DCTCE) on the Peppol network. Understanding it matters because it tells you exactly where the integration work lives.

The five corners (official terminology from MoF Guidelines):

- Corner 1 — Supplier. You generate the invoice in your ERP.

- Corner 2 — Sending ASP. Your Accredited Service Provider validates, converts to UAE XML (PINT-AE / UBL 2.1), transmits on Peppol, and reports Tax Data to the FTA.

- Corner 3 — Receiving ASP. Validates the inbound invoice, delivers to the buyer in their preferred format, and also reports Tax Data to the FTA.

- Corner 4 — Recipient. The buyer auto-processes the invoice in their ERP.

- Corner 5 — Federal Tax Authority (FTA) Central Data Platform. Receives a copy of every transaction in near real time.

Your business is identified on the network by a Peppol Participant Identifier of the form 0235:<TIN>, where the TIN is your 10-digit Tax Identification Number (the first 10 digits of your TRN, if you have one). Each Electronic Invoice also carries a 128-bit UUID generated by the system, in addition to its sequential invoice number.

The legal framework

The mandate is in force. Six instruments to know:

| Instrument | What it does |

|---|---|

| Ministerial Decision No. 243 of 2025 | Defines the Electronic Invoicing System (scope and substantive obligations) |

| Ministerial Decision No. 244 of 2025 | Sets the phased implementation timeline |

| Ministerial Decision No. 64 of 2025 | Eligibility and accreditation procedure for Service Providers |

| Cabinet Decision No. 106 of 2025 | Violations and administrative penalties |

| Ministerial Resolution No. 66 of 2026 | Amends MD 244/2025 — most importantly, extends the ASP-appointment deadline for the AED 50M+ tier (see timeline) |

| Ministerial Resolution No. 56 of 2026 | Amends MD 64/2025 (accreditation procedure) |

Underlying these: VAT Decree-Law (Federal Decree-Law No. 8 of 2017, as amended), Tax Procedures Law (Federal Decree-Law No. 28 of 2022), and the VAT Executive Regulations (Articles 59–60 on invoicing obligations).

Full legislation: mof.gov.ae/en/financial-legislation.

Scope: who is in, who is out

In scope (per MD 243/2025): any Person conducting Business in the UAE — regardless of VAT registration status — for every Business Transaction, unless specifically excluded. This includes non-UAE-established Persons who are obligated to issue Tax Invoices under the VAT Decree-Law.

| Supplier → Buyer | Business | Government | Consumer |

|---|---|---|---|

| Business | B2B ✓ | B2G ✓ | B2C ✗ |

| Government | G2B ✓ | G2G ✓ | G2C ✗ |

| Consumer | C2B ✗ | C2G ✗ | C2C ✗ |

Out of scope (key exclusions):

- Any supply to or from a natural person not acting in business (B2C, G2C, C2*)

- Sovereign activities by Government Entities not in competition with the private sector

- Passenger transportation by Airlines (where an Electronic Ticket is issued)

- Financial services exempt from VAT (Article 42 of the VAT Executive Regulation)

- Imports of Concerned Goods/Services under the reverse charge mechanism

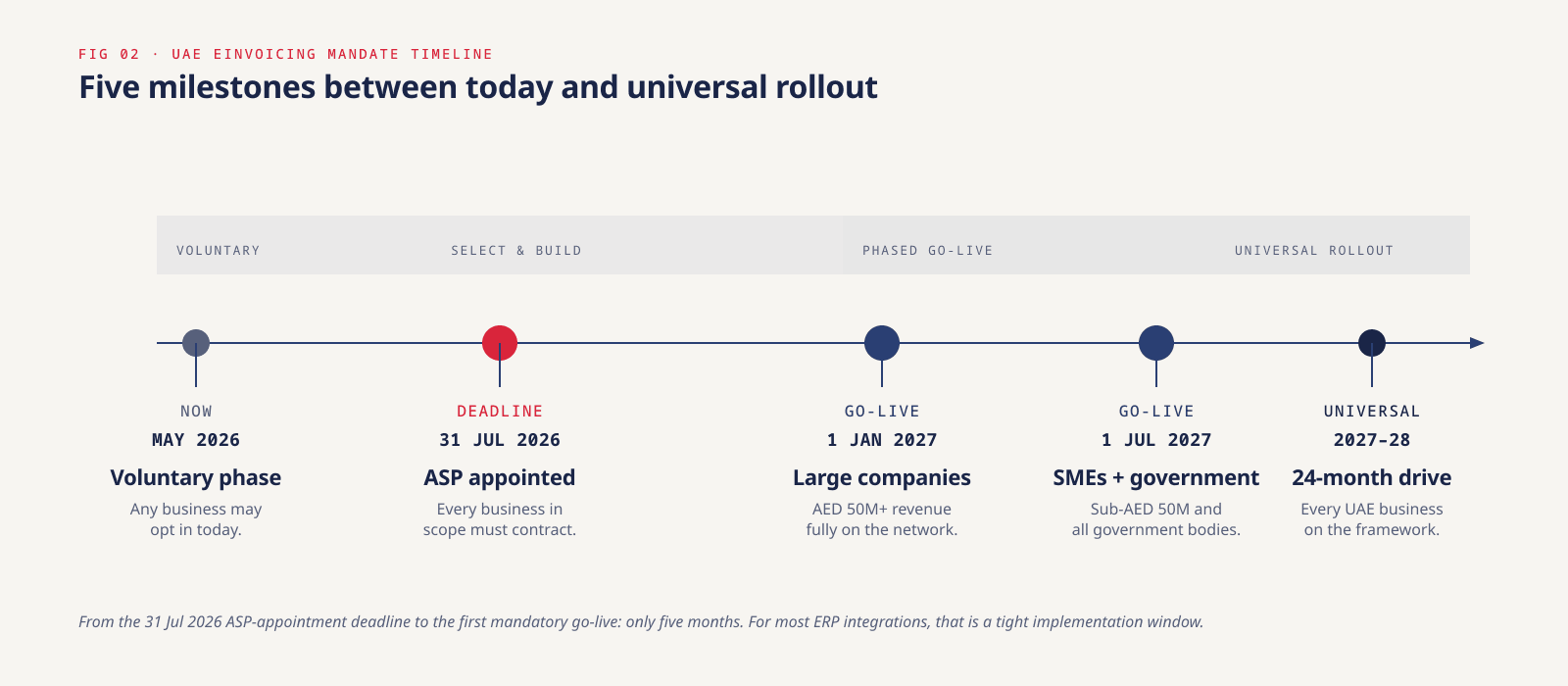

The current timeline

The rollout is phased. The first ASP-appointment deadline has been extended once already (by Ministerial Resolution 66 of 2026); the go-live dates remain unchanged.

The current effective dates:

| Entity | Annual revenue | Appoint an ASP by | Go live by |

|---|---|---|---|

| Person | ≥ AED 50,000,000 | 30 October 2026 (per MR 66/2026; was 31 July 2026) | 1 January 2027 |

| Person | < AED 50,000,000 | 31 March 2027 | 1 July 2027 |

| Government Entity | N/A | 31 March 2027 | 1 October 2027 |

The Pilot Programme and Voluntary phase both commence 1 July 2026. The Ministry contacts pilot participants directly; voluntary participation is open to anyone from that date, with all the same technical requirements and no exposure to penalties until your mandatory date arrives.

The window between selecting an ASP and going live is only two months for large companies. That is not much time to integrate, test, train, and verify.

What your invoices must contain

Every PINT-AE eInvoice must carry the mandatory fields defined in Peppol’s PINT-AE billing specifications and the UAE Data Dictionary. The MoF publishes a separate UAE Electronic Invoice Mandatory Fields document. The fields fall into six categories:

| Category | What it covers | Where master-data gaps usually are |

|---|---|---|

| Invoice header | Number, date, type codes, currency, due date, transaction type | Transaction-type / payment-means codes |

| Seller details | Name, TRN, legal registration, electronic address, address | Electronic address, electronic identifier |

| Buyer details | The same, for your customer | Customer Peppol IDs and TRNs — usually missing in ERP |

| Document totals | Net, tax, gross, payable | Reconciliation logic |

| Tax breakdown | Category, rate, amount per tax category | Category codes (standard / zero / exempt) |

| Line items | Quantity, unit, price, item codes, line VAT in AED | VAT in AED, unit codes |

There are six categories of Electronic Invoices (standard billing: Electronic Tax Invoice, Electronic Tax Credit Note, Commercial Invoice, Electronic Credit Note; self-billing: Self-billed Tax Invoice and Tax Credit Note) and eight named scenarios that add specific requirements: Free Zone, deemed supplies, margin scheme, summary invoices, continuous supplies, agent billing, e-commerce, and exports.

Who does what

Persons issuing invoices must ensure their accounting/ERP/invoicing system can store every required field, generate compliant invoices, connect to an ASP’s API for outbound and inbound, track real-time status, and maintain an audit trail. Modern cloud ERPs (D365 Business Central, S/4HANA, Oracle Fusion) get localisation updates from their vendors. Older or on-premise ERPs — Microsoft Dynamics NAV 2017 and earlier, older SAP versions, bespoke systems — need custom integration.

A Person within scope must appoint only one ASP for both sending and receiving. (VAT Group members each onboard individually with their own TIN and Peppol Participant Identifier; different members may choose different ASPs.)

Accredited Service Providers (ASPs) are MoF-accredited per MD 64/2025. They validate, convert to UAE XML, transmit on Peppol, look up Peppol participant identifiers, generate UUIDs, report Tax Data to the FTA (Corner 5), and forward Message Level Status (MLS) confirmations back through the chain.

Chartered accountants and tax advisors advise clients on appointing ASPs, integrating their ERPs, populating missing master data, and testing before the deadlines. Getting ahead of this proactively is both a service opportunity and reputational protection.

The ERP integration work, in eight steps

Most businesses assume that because their ERP issues invoices today, eInvoicing is a configuration exercise. For cloud ERPs with vendor support, partly true. For everything else it is a custom integration project.

- Gap analysis. Map every required PINT-AE field against what your ERP currently stores. Audit invoice form, customer master, vendor master, company settings.

- Data-model extension. Add what’s missing. Peppol participant identifiers, electronic addresses and buyer tax identifiers don’t exist in vanilla ERPs.

- API integration. Build the connection to your ASP’s API: OAuth 2.0 auth, invoice submission, status polling, inbound retrieval. Technically the heaviest piece.

- Validation engine. Pre-submission checks that flag missing or invalid fields before an invoice is posted, not after.

- Outbound processing. Automate submission of every sales invoice and credit note. Invisible to the user — they post, the system submits.

- Inbound processing. Auto-retrieve purchase invoices and create them in the ERP. The AP-automation upside most teams haven’t thought about.

- Monitoring. Dashboard inside the ERP showing submission volumes, success rates, rejection reasons.

- Audit trail. Log every API interaction with full request/response detail, plus UUIDs and Tax Data Document IDs. Your evidence trail for FTA inspections, retained for 5–7 years per the Tax Procedures Executive Regulation.

Done properly, that’s 6 to 10 weeks of work depending on the ERP and master-data cleanup required.

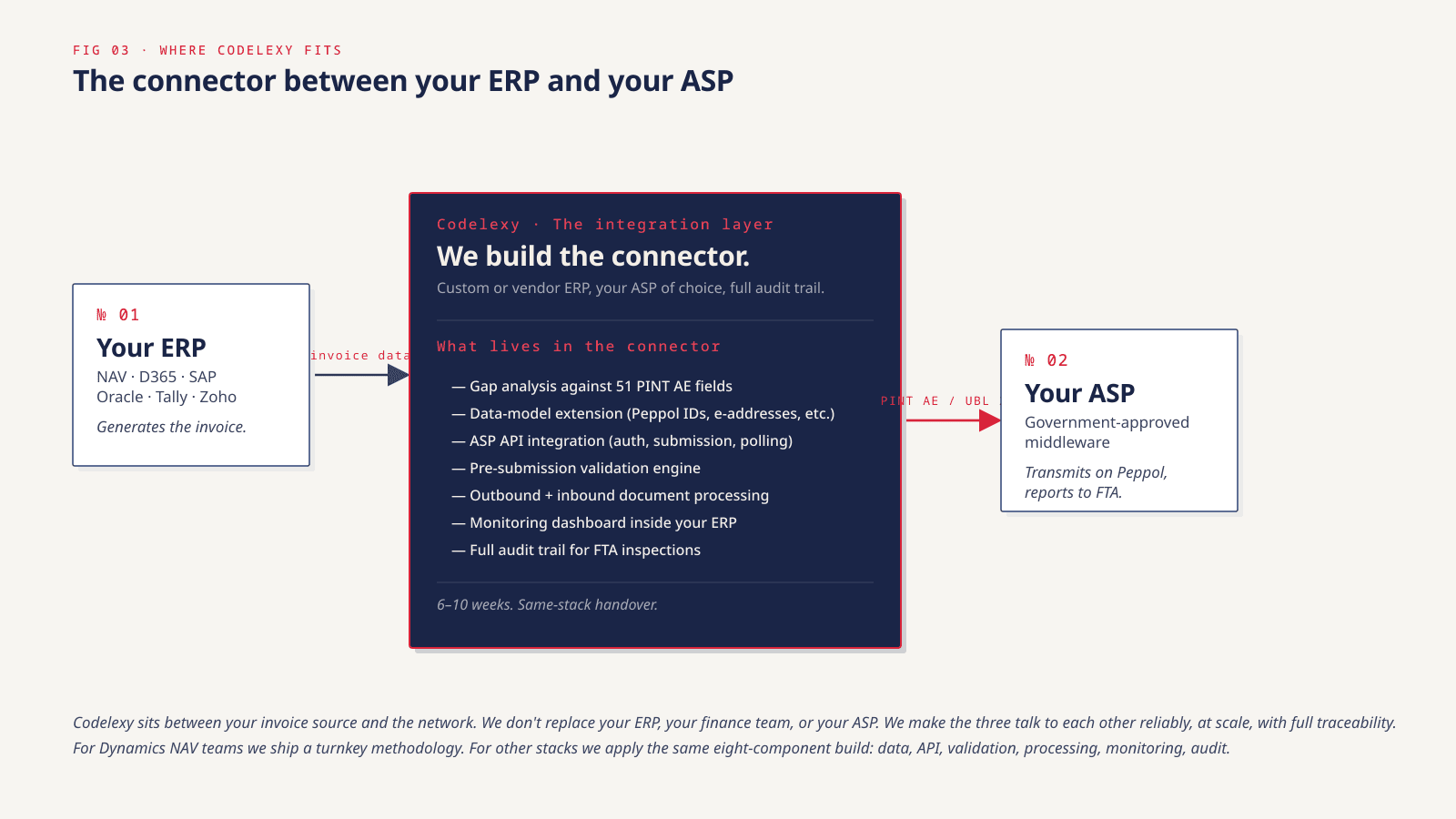

Where Codelexy fits

We work at the intersection of systems integration and compliance. We don’t resell ASP licences. We don’t advise abstractly. We build the connector that makes your ERP compliant.

For Microsoft Dynamics NAV teams we ship a turnkey methodology covering all eight components above — built and validated on real UAE deployments. NAV is one of the largest "older ERP" footprints in the region and the one that needs custom work most acutely.

For other ERP platforms we apply the same structured approach. Gap analysis first. Build second. Test rigorously. Hand over with full documentation and a runbook.

For CAs and tax advisors we partner as the technical implementation layer. Your client gets end-to-end coverage — compliance advice from you, system integration from us.

The handover is the test: when we leave, your finance team posts invoices the same way they always did. The submission, validation and reporting happens silently behind the scenes.

The benefits beyond compliance

Per the MoF, "eInvoicing can significantly reduce invoice processing costs for businesses and governments by up to 66%". Businesses in countries where similar systems have been mandatory for years (Brazil, Mexico, Saudi Arabia, Italy, the Nordic countries) consistently report changes they would not voluntarily give up:

- Faster payment cycles. Invoices land in the customer’s system. No "I didn’t receive it" or "it’s in someone’s inbox".

- Lower rejection rates. Pre-submission validation catches errors before invoices leave your system.

- Reduced AP/AR workload. Manual keying of supplier invoices disappears for any compliant supplier.

- Better audit readiness. A complete, timestamped, government-validated transaction log makes VAT audits much easier.

- Real-time visibility. The gap between what you issued and what the FTA knows shrinks to near zero.

- Pre-populated VAT returns + faster refunds. The MoF expects to streamline the VAT refund mechanism and pre-populate returns from eInvoicing data.

How to choose an ASP

You are handing the ASP the nerve centre of your billing. The MoF’s own Considerations guide (V1.0, Feb 2026) lists the criteria.

Experience and background. How long providing eInvoicing services? How long as a Peppol Service Provider? How long in the UAE? When was the company accredited in the UAE? Live customers on the UAE network or still onboarding? Reference customers in your industry?

Product and service. Their own product or a reseller? Pre-built integrations for your ERP (NAV, SAP, Oracle, Tally, Zoho)? Bidirectional exchange or outbound-only? SLAs for after-hours failures? Pricing model — per-invoice, monthly, enterprise? ISO 27001 certified? Where does your data reside?

On penalties

Cabinet Decision No. 106 of 2025 establishes the penalty framework specifically for Electronic Invoicing violations. Administrative penalties under the existing VAT and Tax Procedures regime (Cabinet Decision No. 40 of 2017) continue to apply for Tax Invoice compliance generally.

A useful clarification: Electronic Invoicing penalties do not apply during the voluntary phase. They apply only from your mandatory implementation date.

Your next steps — a practical checklist

| When | What |

|---|---|

| This week | Confirm your revenue band (AED 50M+, below, or Government); identify the internal owner (Finance, IT, Operations); check your ERP vendor’s UAE PINT-AE roadmap; obtain your TIN via EmaraTax if you don’t have one |

| In 30 days | Review the MoF’s list of accredited ASPs; commission a gap analysis against the PINT-AE field set; assess customer master-data completeness (especially Peppol IDs and TRNs) |

| By 30 June 2026 | Begin ASP evaluation in earnest. The voluntary phase opens 1 Jul 2026 — onboarding early gives you real testing time |

| By 30 October 2026 (large companies) | Selected and contracted with an ASP — this is the mandatory deadline. Initiate onboarding via EmaraTax |

| By 31 March 2027 (SMEs + Government) | Same milestone for the smaller-revenue tier and government entities |

| By 31 October 2026 (large companies) | Integration tested in sandbox; finance team trained; first supervised live submissions |

| 1 January 2027 | Large companies fully live. Every in-scope sales invoice and credit note issuing through Peppol |

| 1 July 2027 | SMEs (< AED 50M) fully live |

| 1 October 2027 | Government entities fully live |

Frequently asked questions

We use Tally / Zoho Books / QuickBooks. Do we need to change software?

Not necessarily. The requirement is on the network and format, not the software. Some ASPs offer web portals for manual eInvoice submission — fine for low volumes. Above ~20–30 invoices/month, a direct ERP integration pays for itself in saved manual effort.

We only sell to consumers (B2C). Does this apply?

No. The mandate covers B2B, B2G, G2B and G2G. Supplies to natural persons not in business are out of scope. The MoF may extend scope in future phases.

Our customers are outside the UAE. Do we still need to eInvoice them?

Yes if the supplier is in the UAE and a Tax Invoice is required under the VAT Decree-Law. Where the buyer has no Peppol ID, the supplier includes the predefined endpoint 0235:9900000099 on the Electronic Invoice.

What is a Peppol participant identifier, and how do we get one?

It’s a unique electronic identifier on the Peppol network of the form 0235:<10-digit TIN>. Your TIN is the first 10 digits of your TRN (issued by the FTA). Your ASP registers your Peppol Participant Identifier when you onboard.

We are a free-zone company. Does the mandate apply?

Yes if you conduct Business in the UAE. Free Zone transactions are in scope, with an additional requirement to capture the beneficiary on the Electronic Invoice.

We’re a VAT group. How does this work?

Each Tax Group member onboards individually with its own TIN and Peppol Participant Identifier — they may even pick different ASPs. Intra-group transactions are deferred by 24 months from 1 January 2027 (no compliance required during that grace period).

Can we use more than one ASP?

A single Person must appoint only one ASP for both sending and receiving. Different members of a VAT group, however, may use different ASPs.

Closing thought

The UAE eInvoicing mandate is the most significant change to business administration in the UAE in the past decade. For all but the simplest setups the technical work is substantial enough that starting now is the only way to be comfortable by the deadline.

The businesses that will struggle are the ones that treat this as a last-minute IT project. The businesses that will benefit are the ones that treat it as an opportunity to modernise invoicing, clean up data, and automate processes that have been run manually for years.

The regulation is fixed. The deadline is fixed. What you control is how prepared you are when it arrives.

Sources: UAE Ministry of Finance (eInvoicing initiative, UAE Electronic Invoicing Guidelines V1.0 of 23 February 2026, Considerations for Selecting an ASP V1.0), Federal Tax Authority (tax.gov.ae), OpenPeppol (peppol.org). This article is informational and does not constitute legal or tax advice. Consult a qualified advisor for guidance specific to your business.